Vicky26's latest activity

-

VVicky26 posted the thread Netting, Close-out and Related Aspects in P2.T6. Credit Risk Measurement & Management.The opposite signs of MTM is due to fact that each party owes some amount to another. Say A & B, where A defaults. A owed 20 to B and B...

-

-

VVicky26 replied to the thread Hull, Options, Futures, and Other Derivatives, Chapter 24.In that case why are we doing '1 minus' in formula for V(T,X). It should just be formula for WCDR, and no '1 minus'.

-

VVicky26 posted the thread Hull, Options, Futures, and Other Derivatives, Chapter 25 in P2.T6. Credit Risk Measurement & Management.I dont understand this logic. If CDS spread>bond yield, then how is buy bond and buy CDS better. If CDS pread is 170bps and bond yield =...

-

-

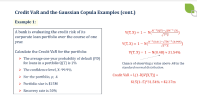

VVicky26 posted the thread Hull, Options, Futures, and Other Derivatives, Chapter 24 in P2.T6. Credit Risk Measurement & Management.Vasicek model gives WCDR which is same as 1-V(T,X). Then why are we using V(T,X) while calculating Credit VAR. Formula for credit VAR...

-

-

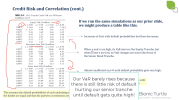

VVicky26 posted the thread Chapter 9: Structured Credit Risk in P2.T6. Credit Risk Measurement & Management.Why is VAR value so high for Senior Tranche ?

-

-

VVicky26 replied to the thread P2-T6-Malz, Chapter 8: Portfolio Credit Risk.Its in the video for Portfolio Credit Risk and tutor refers to the link that can be used to access detailed video on Copula.

-

VVicky26 replied to the thread P2-T6-Malz, Chapter 8: Portfolio Credit Risk.I got the video for Portfolio Credit Risk. I am asking about the copula video which is referenced to in the video (encircled in red in...

-

VVicky26 posted the thread P2-T6-Malz, Chapter 8: Portfolio Credit Risk in P2.T6. Credit Risk Measurement & Management.Where can we get link to the Copula video?

-

-

VVicky26 posted the thread Hull, Chapter 19. Credit Value at Risk in P2.T6. Credit Risk Measurement & Management.for BBB to B calculation for PV is at t=1month which is compared with current price which is at t=0. Shouldn't the time frame be same...

-