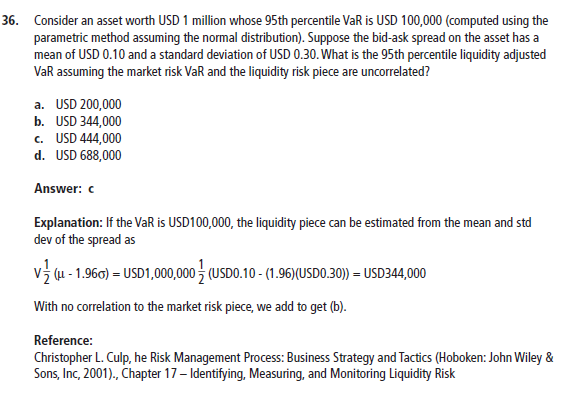

This is a circulating question on liquidity-adjusted value at risk (LVaR) that several members have submitted over the years (image source: a member posted elsewhere in the general forum):

At least one mistake has been confirmed!

Question: what is the correct 95% LVaR answer (hint: it is not given as an option)?

At least one mistake has been confirmed!

Question: what is the correct 95% LVaR answer (hint: it is not given as an option)?