Normally we think of solving for the call option given the inputs (risk factors), where volatility is a key input:

call option = BlackScholes[stock, strick, volatility,...]

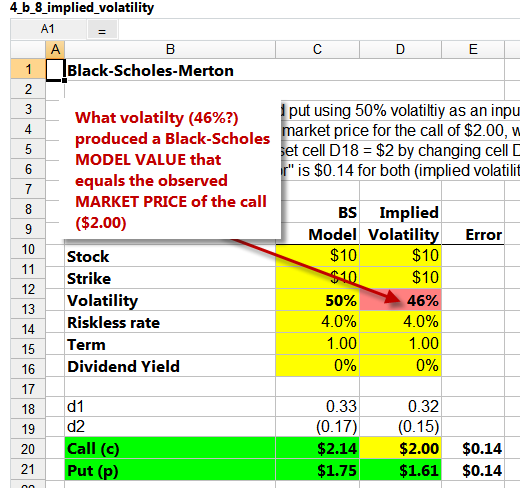

implied vol is "reverse engineering" where (i) we have a traded market price and (ii) a OPM model, such that we find the volatility that returns a model price equal to the observed market price.

So in the XLS (screenshot below), you have to *iterate* or *goal-seek* to find it, but let's assume you *observe* the call option trades at $2.00 (see Call (c) = $2.0 in second column), then you goal seek or find the volatility that returns the $2 option price. In this case, 46% works. So, we say:

"the market price of $2 implies a volatility of 46%"

our concern is the volatility smile (or smirk, as my colleagues used to say!) that is assigned Chapter 18 Hull...this movie tutorial is next to be published!

This site uses cookies to help personalise content, tailor your experience and to keep you logged in if you register.

By continuing to use this site, you are consenting to our use of cookies.

{kind=link}