mikey10011

New Member

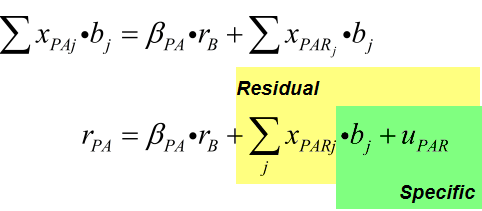

I am missing something with the substitutions so could you go through step-by-step equations 17.20 through 17.23 in Grinold (p. 500)? Also could you provide some insight or interpretation of the mathematical manipulations? For example where did u_PAR(t) in Eq. 17.23 come from?

Note that I bought Grinold Chapter 17 from GARP but the whole book is online with Google books (e.g., r_B(t) = benchmark return defined on p. 29). So feel free to refer to other pages outside of the chapter.

Note that I bought Grinold Chapter 17 from GARP but the whole book is online with Google books (e.g., r_B(t) = benchmark return defined on p. 29). So feel free to refer to other pages outside of the chapter.

{kind=link}