Learning objectives: Define derivatives, describe the features and uses of derivatives and compare linear and non-linear derivatives. Describe the specifics of exchange-traded and over-the-counter markets, and evaluate the advantages and disadvantages of each. Differentiate between options, forwards, and futures contracts. Identify and calculate option and forward contract payoffs. Differentiate among the broad categories of traders: hedgers, speculators, and arbitrageurs.

Questions:

21.8.1. Eddie is a retail investor who believes that Starbucks (ticker: SBUX), which is a dividend-paying stock (its dividend yield is currently ~1.75%), is an attractive long-term business. He would like to own SBUX shares over a long horizon (i.e., at least three years), but at the same time, he considers the stock to be currently overpriced by ~15% due to the market's temporary euphoria. Specifically, SBUX trades today at $115.00 but Eddie wants to buy the stock only if its price drops below $100.00 because he believes its current intrinsic value is $100.00. Under this view, Eddie has a long-term bullish view but he wants a lower entry price if it becomes possible in the near term due to a market dip or correction. This is why he will not buy the stock today. Finally, rather than make an initial investment, he prefers to receive up-front cash flow.

Eddie wonders if a naked option trade can express his view. Given his views and preferences, among these naked option trades, which of the following option trades is best for him?

a. Buy out-of-the-money calls

b. Sell in-the-money calls

c. Buy in-the-money puts

d. Sell out-of-the-money puts

21.8.2. Unaholding FinServices Corporation last quarter entered into a derivative contract that has since become a relatively large position. In response to a query by the Board's Risk Committee, the Chief Financial Officer (CFO) makes the argument that the derivate trade is a hedge, rather than a speculation or an arbitrage. Which of the following is the best support for her argument that the trade is a hedge?

a. The potential loss on the derivative contract itself is capped (aka, limited) to a 25% loss

b. The derivative's initial value was zero and trade is considered non-directional or range-bound

c. The derivative's value is highly correlated (negatively or positively) to an underlying exposure at the corporation

d. The net position (the derivative plus an underlying exposure) eliminates all risks; i.e., the net position is without risk

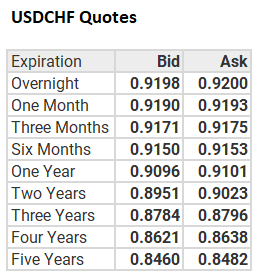

21.8.3. Swissmaker Corporation (who is based in Switzerland) entered into a contract with a key vendor in the United States and will need to deliver $1.0 million (USD) dollars in two (2) years as payment. Below is displayed the spot and forward exchange rate quotes for USDCHF currency pair (per convention, USD is the base and CHF is the quote currency).

What is the currency risk and what is the (implied) appropriate hedge trade for Swissmaker Corporation?

a. The risk is Swiss Franc (CHF) depreciation, and the hedge is a forward to buy $1.0 million dollars in exchange for 902,300 Swiss Francs

b. The risk is Swiss Franc (CHF) depreciation, and the hedge is a forward to buy $1.0 million dollars in exchange for 1,108,279 Swiss Francs

c. The risk is Swiss Franc (CHF) appreciation, and the hedge is a forward to sell $1.0 million dollars in exchange for 1,117,194 Swiss Francs

d. The risk is Swiss Franc (CHF) appreciation, and the hedge is a forward to sell $1.0 million dollars in exchange for 895,100 Swiss Francs

Answers here:

Questions:

21.8.1. Eddie is a retail investor who believes that Starbucks (ticker: SBUX), which is a dividend-paying stock (its dividend yield is currently ~1.75%), is an attractive long-term business. He would like to own SBUX shares over a long horizon (i.e., at least three years), but at the same time, he considers the stock to be currently overpriced by ~15% due to the market's temporary euphoria. Specifically, SBUX trades today at $115.00 but Eddie wants to buy the stock only if its price drops below $100.00 because he believes its current intrinsic value is $100.00. Under this view, Eddie has a long-term bullish view but he wants a lower entry price if it becomes possible in the near term due to a market dip or correction. This is why he will not buy the stock today. Finally, rather than make an initial investment, he prefers to receive up-front cash flow.

Eddie wonders if a naked option trade can express his view. Given his views and preferences, among these naked option trades, which of the following option trades is best for him?

a. Buy out-of-the-money calls

b. Sell in-the-money calls

c. Buy in-the-money puts

d. Sell out-of-the-money puts

21.8.2. Unaholding FinServices Corporation last quarter entered into a derivative contract that has since become a relatively large position. In response to a query by the Board's Risk Committee, the Chief Financial Officer (CFO) makes the argument that the derivate trade is a hedge, rather than a speculation or an arbitrage. Which of the following is the best support for her argument that the trade is a hedge?

a. The potential loss on the derivative contract itself is capped (aka, limited) to a 25% loss

b. The derivative's initial value was zero and trade is considered non-directional or range-bound

c. The derivative's value is highly correlated (negatively or positively) to an underlying exposure at the corporation

d. The net position (the derivative plus an underlying exposure) eliminates all risks; i.e., the net position is without risk

21.8.3. Swissmaker Corporation (who is based in Switzerland) entered into a contract with a key vendor in the United States and will need to deliver $1.0 million (USD) dollars in two (2) years as payment. Below is displayed the spot and forward exchange rate quotes for USDCHF currency pair (per convention, USD is the base and CHF is the quote currency).

What is the currency risk and what is the (implied) appropriate hedge trade for Swissmaker Corporation?

a. The risk is Swiss Franc (CHF) depreciation, and the hedge is a forward to buy $1.0 million dollars in exchange for 902,300 Swiss Francs

b. The risk is Swiss Franc (CHF) depreciation, and the hedge is a forward to buy $1.0 million dollars in exchange for 1,108,279 Swiss Francs

c. The risk is Swiss Franc (CHF) appreciation, and the hedge is a forward to sell $1.0 million dollars in exchange for 1,117,194 Swiss Francs

d. The risk is Swiss Franc (CHF) appreciation, and the hedge is a forward to sell $1.0 million dollars in exchange for 895,100 Swiss Francs

Answers here:

Last edited by a moderator: