Learning objectives: Describe the relationship between stress testing and other risk measures, particularly in enterprise-wide stress testing. Describe the various approaches to using VaR models in stress tests. Explain the importance of stressed inputs and their importance in stressed VaR. Identify the advantages and disadvantages of stressed risk metrics.

Questions:

802.1. Siddique and Hasan compare and contrast stress testing with economic capital and value at risk measures (aka, EC/VaR methods). In regard to key differences between the methods, each of the following statement accurately summarizes a distinction EXCEPT which statement is inaccurate?

a. In practice stress tests often take an accounting view rather than the market view that is common in EC/VaR methods

b. With respect to time horizon, enterprise-wide stress tests often examine a long period (e.g., nine quarters); in contrast, VaR/EC models tend to focus on a point in time (e.g., end of year).

c. EC/VaR methods generate loss estimates for portfolios but are not well-suited as enterprise-wide measures; on the other hand, enterprise-wide stress tests are common but they are not good at generating loss estimates

d. Stress-test scenarios are often ad hoc, conditional and make ordinal rank assignments (e.g., base, adverse, severely adverse); in contrast, EC/VaR metrics often generate unconditional scenarios and employ cardinal probabilities

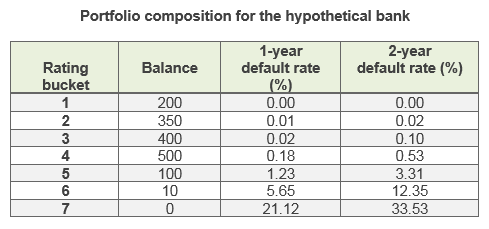

802.2. Shown below is a bank's portfolio of wholesale exposures (this is Siddique and Hasan's Table 2.2):

The bank needs to estimate the sensitivities of this portfolio's losses to changes in two macro variables: gross domestic product (GDP) growth and unemployment. If the bank conducts a stress test, each of the following is likely--or at least reasonable--to be included in the bank's stress test assumptions EXCEPT which is the LEAST likely to be an assumption in the stress test?

a. An abrupt drop in exposures (EAD); e.g., EADs drop by 30.0%

b. Transition to lower rating buckets; e.g., $500 million transitions to Rating 7

c. Stressed default probabilities (PDs); e.g., for Rating bucket 3 the PD spikes to 4.0%

d. Stressed loss given default (LGD); e.g., LGD increases by 10.0% for all rating buckets

802.3. In regard to the importance of stressed inputs in stressed value at risk (VaR), Siddique and Hasan write, "Another approach to incorporating stress into risk measurement methodologies has been the use of stressed inputs. There have been quite a few variants. This has been particularly useful in market risk area. The incorporation of stress into the risk measurement as well as capital metrics has occurred in both the supervisory approaches and the many banks’ internal approaches." They proceed to illustrate a stressed VaR by simulating exposures over two separate 180-day periods, one of which ends June 30th, 2009, and with six factors: (1) Three-month LIBOR (LIBOR3M); (2) the yield on BAA-rated bonds (BAA); (3) the spread between yields on BAA- and AAA-rated bonds (BAA–AAA); (4) the return on the S&P 500 index (SPX); (5) the change in the volatility option index (VIX); and (6) contract interest rates on commitments for fixed-rate first mortgages (MORTG).

This simulation produces stressed risk metrics: both a stressed VaR, and a stressed CVA VaR. Which of the following is a TRUE statement about the genuine DISADVANTAGE of relying on on these stressed risk metrics?

a. Capital is unlikely to be adequate when the next stress or shock occurs

b. The risk metrics will not be responsive to the current market conditions

c. The risk metrics with a stressed input will be more conservative (less aggressive)

d. The risk metrics with a stressed input will be less conservative (more aggressive)

Answers here:

Questions:

802.1. Siddique and Hasan compare and contrast stress testing with economic capital and value at risk measures (aka, EC/VaR methods). In regard to key differences between the methods, each of the following statement accurately summarizes a distinction EXCEPT which statement is inaccurate?

a. In practice stress tests often take an accounting view rather than the market view that is common in EC/VaR methods

b. With respect to time horizon, enterprise-wide stress tests often examine a long period (e.g., nine quarters); in contrast, VaR/EC models tend to focus on a point in time (e.g., end of year).

c. EC/VaR methods generate loss estimates for portfolios but are not well-suited as enterprise-wide measures; on the other hand, enterprise-wide stress tests are common but they are not good at generating loss estimates

d. Stress-test scenarios are often ad hoc, conditional and make ordinal rank assignments (e.g., base, adverse, severely adverse); in contrast, EC/VaR metrics often generate unconditional scenarios and employ cardinal probabilities

802.2. Shown below is a bank's portfolio of wholesale exposures (this is Siddique and Hasan's Table 2.2):

The bank needs to estimate the sensitivities of this portfolio's losses to changes in two macro variables: gross domestic product (GDP) growth and unemployment. If the bank conducts a stress test, each of the following is likely--or at least reasonable--to be included in the bank's stress test assumptions EXCEPT which is the LEAST likely to be an assumption in the stress test?

a. An abrupt drop in exposures (EAD); e.g., EADs drop by 30.0%

b. Transition to lower rating buckets; e.g., $500 million transitions to Rating 7

c. Stressed default probabilities (PDs); e.g., for Rating bucket 3 the PD spikes to 4.0%

d. Stressed loss given default (LGD); e.g., LGD increases by 10.0% for all rating buckets

802.3. In regard to the importance of stressed inputs in stressed value at risk (VaR), Siddique and Hasan write, "Another approach to incorporating stress into risk measurement methodologies has been the use of stressed inputs. There have been quite a few variants. This has been particularly useful in market risk area. The incorporation of stress into the risk measurement as well as capital metrics has occurred in both the supervisory approaches and the many banks’ internal approaches." They proceed to illustrate a stressed VaR by simulating exposures over two separate 180-day periods, one of which ends June 30th, 2009, and with six factors: (1) Three-month LIBOR (LIBOR3M); (2) the yield on BAA-rated bonds (BAA); (3) the spread between yields on BAA- and AAA-rated bonds (BAA–AAA); (4) the return on the S&P 500 index (SPX); (5) the change in the volatility option index (VIX); and (6) contract interest rates on commitments for fixed-rate first mortgages (MORTG).

This simulation produces stressed risk metrics: both a stressed VaR, and a stressed CVA VaR. Which of the following is a TRUE statement about the genuine DISADVANTAGE of relying on on these stressed risk metrics?

a. Capital is unlikely to be adequate when the next stress or shock occurs

b. The risk metrics will not be responsive to the current market conditions

c. The risk metrics with a stressed input will be more conservative (less aggressive)

d. The risk metrics with a stressed input will be less conservative (more aggressive)

Answers here: