Learning objectives: Define, compute, and interpret the effective duration of a fixed income security given a change in yield and the resulting change in price. Compare and contrast DV01 and effective duration as measures of price sensitivity. Define, compute, and interpret the convexity of a fixed income security given a change in yield and the resulting change in price.

Questions:

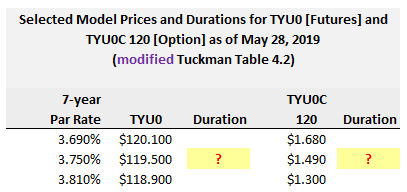

909.1. The exhibit below modifies Tuckman's Table 4.2 and shows the prices on May 28, 2019 for two instruments: 10-year U.S. note futures contracts, TYU0, and call options with a strike of 120 on the same futures contracts, TYU0C 120.

(Bruce Tuckman, Fixed Income Securities, 3rd Edition (Hoboken, NJ: John Wiley & Sons, 2011))

What is the effective duration of, respectively, the futures, TYU0, and the options, TYU0C 120?

a. 4.2 and 106.3 years

b. 8.4 and 212.5 years

c. 33.5 and 850.1 years

d. 41.8 and 1,062.6 years

909.2. Each of the following is true EXCEPT

a. If a bond's DV01 is a continually decreasing function of the interest rate, then its price/rate curve is always positively convex

b. Effective duration can assume any change in the term structure of interest rates; i.e., it does not require yield as the interest rate factor

c. If the first derivative of a bond's price with respect to yield (aka, dollar duration) is negative, then the price/rate curve exhibits negative convexity at that point

d. If the first derivative of a bond's price with respect to yield (aka, dollar duration) is an increasing function of the interest rate, then its price/rate curve is always positively convex

909.3. A speculative (aka, junk) bond has 15.0 years to maturity and pays a semi-annual 6 1/8 coupon; i.e., its coupon rate is 6.125% payable semi-annually. Its yield is 11.00%. If we assume a reasonable shock value (i.e., less than 100 basis points), which of the following is nearest to the bond's effective convexity?

a. 12.4 years^2

b. 98.0 years^2

c. 124.3 years^2

d. Cannot answer because face value is not given

Answers here:

Questions:

909.1. The exhibit below modifies Tuckman's Table 4.2 and shows the prices on May 28, 2019 for two instruments: 10-year U.S. note futures contracts, TYU0, and call options with a strike of 120 on the same futures contracts, TYU0C 120.

(Bruce Tuckman, Fixed Income Securities, 3rd Edition (Hoboken, NJ: John Wiley & Sons, 2011))

What is the effective duration of, respectively, the futures, TYU0, and the options, TYU0C 120?

a. 4.2 and 106.3 years

b. 8.4 and 212.5 years

c. 33.5 and 850.1 years

d. 41.8 and 1,062.6 years

909.2. Each of the following is true EXCEPT

a. If a bond's DV01 is a continually decreasing function of the interest rate, then its price/rate curve is always positively convex

b. Effective duration can assume any change in the term structure of interest rates; i.e., it does not require yield as the interest rate factor

c. If the first derivative of a bond's price with respect to yield (aka, dollar duration) is negative, then the price/rate curve exhibits negative convexity at that point

d. If the first derivative of a bond's price with respect to yield (aka, dollar duration) is an increasing function of the interest rate, then its price/rate curve is always positively convex

909.3. A speculative (aka, junk) bond has 15.0 years to maturity and pays a semi-annual 6 1/8 coupon; i.e., its coupon rate is 6.125% payable semi-annually. Its yield is 11.00%. If we assume a reasonable shock value (i.e., less than 100 basis points), which of the following is nearest to the bond's effective convexity?

a. 12.4 years^2

b. 98.0 years^2

c. 124.3 years^2

d. Cannot answer because face value is not given

Answers here: