Learning objectives: Describe how mapping of risk factors can support stress testing. Explain how VaR can be used as a performance benchmark.

Questions:

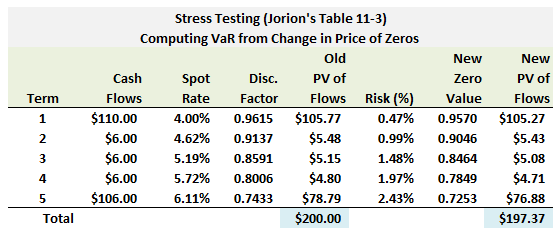

716.1. The table below exhibits Jorion's stress test of a $200.0 million two-bond portfolio: one bond is a $100.0 million 5-year 6.0% annual coupon issue, and the second bond is a $100.0 million 1-year 4.0% annual coupon issue.

(Source: Philippe Jorion, Value-at-Risk: The New Benchmark for Managing Financial Risk, 3rd Edition (New York: McGraw Hill, 2006))

Each of the following statements about this stress test exercise is true EXCEPT which is false?

a. The stressed portfolio loss is about $2.63 million

b. Because this stress test does not utilize mapping to risk factors such that the VaRs of the zero-coupon bond vertexes are not utilized, this stress is essentially a simulation achieved by fully re-pricing the portfolio's component bonds

c. The stressed portfolio loss is equal to the undiversified portfolio value at risk (VaR) because the implicit assumption in the stress test is that all zeros are perfectly correlated

d. The stressed portfolio loss will increase if either the confidence level is increased and/or the underlying yield volatility assumptions (e.g., 1-year or 5-year basis point volatility) are increased

716.2. A portfolio manager enters a 7.0 year pay-fixed swap with notional of $100.0 million. The (modified) duration of the fixed leg is 5.90 years, and the floating leg has just been reset for payment in a year. Assume a flat term structure and an annual volatility of yield changes of 100 basis points. What is the portfolio manager's 99.0% value at risk (VaR) over the next month? (note: this is a variation on Jorion's EOC Question 11.9). (Philippe Jorion, Value-at-Risk: The New Benchmark for Managing Financial Risk, 3rd Edition (New York: McGraw Hill, 2006))

a. Zero (the portfolio manager is the fixed payer)

b. $2.80 million

c. $3.30 million

d. $11.42 million

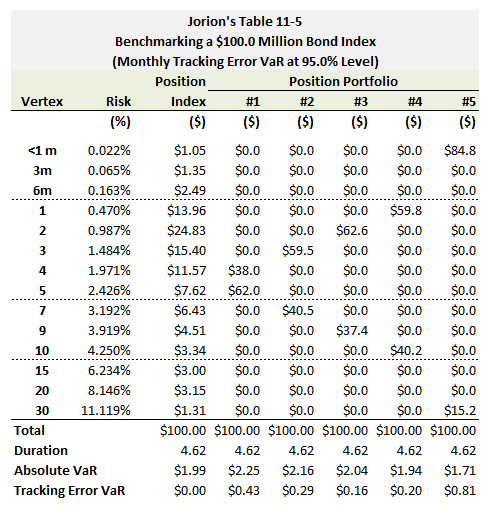

716.3. The table below recreates Jorion's table (11-5) that provides an example of benchmarking a $100.0 million bond portfolio against a performance benchmark; the benchmark is presumed to be the J.P. Morgan U.S. bond index (column "Position Index"). (Source: Philippe Jorion, Value-at-Risk: The New Benchmark for Managing Financial Risk, 3rd Edition (New York: McGraw Hill, 2006))

(Source: Philippe Jorion, Value-at-Risk: The New Benchmark for Managing Financial Risk, 3rd Edition (New York: McGraw Hill, 2006))

About this benchmarking exercising, each of the following statements is true EXCEPT which is false?

a. If the goal is generally to minimize risk, then Position Portfolios one and two (#1 and #2) are superior to the others

b. The barbell portfolio offers the lowest absolute risk and this is consistent with lower correlations for more distant maturities

c. Relative to the original index, the variance improvement obtained by the first portfolio (#1) is about 1 - (0.43/1.99)^2 = 95.4%

d. If the goal is to minimize tracking error tracking error risk and come nearest to approximating the cash-flow positions in the index, the best Position Portfolio is three (#3)

Answers here:

Questions:

716.1. The table below exhibits Jorion's stress test of a $200.0 million two-bond portfolio: one bond is a $100.0 million 5-year 6.0% annual coupon issue, and the second bond is a $100.0 million 1-year 4.0% annual coupon issue.

(Source: Philippe Jorion, Value-at-Risk: The New Benchmark for Managing Financial Risk, 3rd Edition (New York: McGraw Hill, 2006))

Each of the following statements about this stress test exercise is true EXCEPT which is false?

a. The stressed portfolio loss is about $2.63 million

b. Because this stress test does not utilize mapping to risk factors such that the VaRs of the zero-coupon bond vertexes are not utilized, this stress is essentially a simulation achieved by fully re-pricing the portfolio's component bonds

c. The stressed portfolio loss is equal to the undiversified portfolio value at risk (VaR) because the implicit assumption in the stress test is that all zeros are perfectly correlated

d. The stressed portfolio loss will increase if either the confidence level is increased and/or the underlying yield volatility assumptions (e.g., 1-year or 5-year basis point volatility) are increased

716.2. A portfolio manager enters a 7.0 year pay-fixed swap with notional of $100.0 million. The (modified) duration of the fixed leg is 5.90 years, and the floating leg has just been reset for payment in a year. Assume a flat term structure and an annual volatility of yield changes of 100 basis points. What is the portfolio manager's 99.0% value at risk (VaR) over the next month? (note: this is a variation on Jorion's EOC Question 11.9). (Philippe Jorion, Value-at-Risk: The New Benchmark for Managing Financial Risk, 3rd Edition (New York: McGraw Hill, 2006))

a. Zero (the portfolio manager is the fixed payer)

b. $2.80 million

c. $3.30 million

d. $11.42 million

716.3. The table below recreates Jorion's table (11-5) that provides an example of benchmarking a $100.0 million bond portfolio against a performance benchmark; the benchmark is presumed to be the J.P. Morgan U.S. bond index (column "Position Index"). (Source: Philippe Jorion, Value-at-Risk: The New Benchmark for Managing Financial Risk, 3rd Edition (New York: McGraw Hill, 2006))

(Source: Philippe Jorion, Value-at-Risk: The New Benchmark for Managing Financial Risk, 3rd Edition (New York: McGraw Hill, 2006))

About this benchmarking exercising, each of the following statements is true EXCEPT which is false?

a. If the goal is generally to minimize risk, then Position Portfolios one and two (#1 and #2) are superior to the others

b. The barbell portfolio offers the lowest absolute risk and this is consistent with lower correlations for more distant maturities

c. Relative to the original index, the variance improvement obtained by the first portfolio (#1) is about 1 - (0.43/1.99)^2 = 95.4%

d. If the goal is to minimize tracking error tracking error risk and come nearest to approximating the cash-flow positions in the index, the best Position Portfolio is three (#3)

Answers here:

Last edited: