AIMs: Identify common types of structured products and the various dimensions that are important to their value and structure. Describe the role of capital structure and credit losses in a securitization. Evaluate a waterfall example in a securitization with multiple tranches. Identify the key participants in a securitization, and describe some conflicts of interest that can arise in the process.

Questions:

312.1. Each of the following is a valid DIFFERENCE between between a Covered Bond and a "true securitization" (Malz's term) except which is NOT TRUE?

a. In a covered bond, the cover pool remains on the balance sheet; but in a true securitization, loans (assets) are removed from the balance sheet

b. In a covered bond, principal and interest (P&I) are paid from issuer's general cash flows; but in a securitization, P&I are paid from the collateral pool directly

c. Unlike a true securitization, there is NOT a "true sale" of assets to a bankruptcy-remote special purpose vehicle in the case of a covered bond

d. Unlike a true securitization, a covered bond neither create securities nor is a genuine method for raising funds (i.e., borrowing) in capital markets

312.2. Assume a collateralized loan obligation (CLO) which has as underlying assets 100 identical leveraged loans, with a par value of $1.0 million each, and priced at par. The loans are floating rate obligations that pay a fixed spread of 300 basis points over one-month LIBOR. Assume further there are no upfront, management, or trustee fees. The capital structure consists of a senior bond, a junior bond, and an equity tranche:

a. Negative due to the high junior coupon

b. $350,000

c. $1.70 million

d. $3.49 million

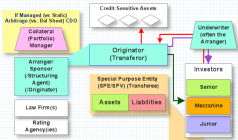

312.3. In a securitization, which key participant is most likely to incur warehousing risk?

a. Originator

b. Underwriter

c. Rating Agency

d. Servicer

Answers:

Questions:

312.1. Each of the following is a valid DIFFERENCE between between a Covered Bond and a "true securitization" (Malz's term) except which is NOT TRUE?

a. In a covered bond, the cover pool remains on the balance sheet; but in a true securitization, loans (assets) are removed from the balance sheet

b. In a covered bond, principal and interest (P&I) are paid from issuer's general cash flows; but in a securitization, P&I are paid from the collateral pool directly

c. Unlike a true securitization, there is NOT a "true sale" of assets to a bankruptcy-remote special purpose vehicle in the case of a covered bond

d. Unlike a true securitization, a covered bond neither create securities nor is a genuine method for raising funds (i.e., borrowing) in capital markets

312.2. Assume a collateralized loan obligation (CLO) which has as underlying assets 100 identical leveraged loans, with a par value of $1.0 million each, and priced at par. The loans are floating rate obligations that pay a fixed spread of 300 basis points over one-month LIBOR. Assume further there are no upfront, management, or trustee fees. The capital structure consists of a senior bond, a junior bond, and an equity tranche:

- The senior debt principal value is $75.0 million and pays an annual coupon of LIBOR plus 100 basis points,

- The junior (mezzanine) debt principal value is $15.0 million and pays an annual coupon of LIBOR plus 500 basis points

a. Negative due to the high junior coupon

b. $350,000

c. $1.70 million

d. $3.49 million

312.3. In a securitization, which key participant is most likely to incur warehousing risk?

a. Originator

b. Underwriter

c. Rating Agency

d. Servicer

Answers: