AIMs: Evaluate one or two iterations of interim cashflows in a three-tiered securitization structure including the final cashflows to each tranche holder.

Questions:

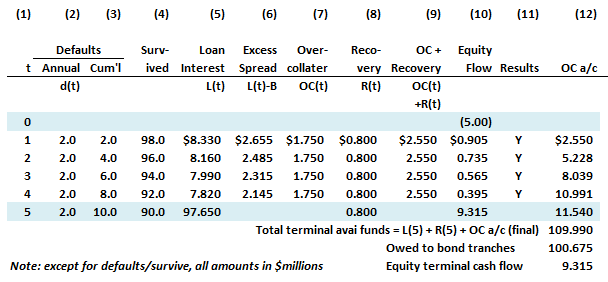

313.1. Let's assume the same three-tier securitization structure illustrated by Malz section 9.2 with identical assumptions, for convenience:

(Source: Allan Malz, Financial Risk Management: Models, History, and Institutions (Hoboken, NJ: John Wiley & Sons, 2011))

Each of the following is true about this structure EXCEPT for which is not?

a. This structure is paying interest to the bondholders of $5.6750 million in each of the five years plus principal repayment in the fifth (5th) year

b. The annual amount diverted to the overcollateralization account is capped at $1.750 million (must be the case, according to the exhibit)

c. The recovery assumption is 40% (must be the case, according to the exhibit)

d. Recovered funds are flowing each year, immediately as recovered, to the equity holders

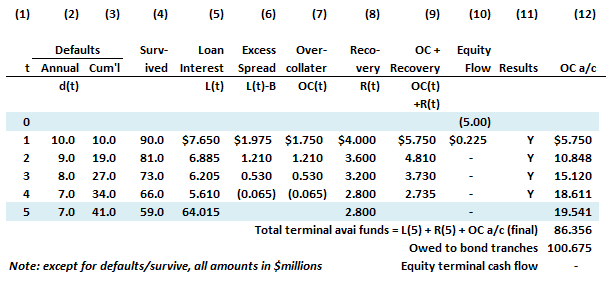

313.2. The following structure is identical to the previous (and to Malz's illustration in section 9.2) but with one difference: in this scenario, the default rate has been dramatically increased to 10.0% per annum:

(Source: Allan Malz, Financial Risk Management: Models, History, and Institutions (Hoboken, NJ: John Wiley & Sons, 2011))

Under this high-default scenario, which of the following statements is true?

a. There is never a year in which either the junior or senior bonds are paid their full interest

b. Both bond holders (senior and junior) realize all of their interest payments in the first four years, but neither recover their entire obligation in the fifth year (i.e., shortfall for both bond holders)

c. Junior bond holder suffer interest payment shortfalls and a principal shortfall, but senior bond holders receive all of their interest and experience no principal shortfall

d. Both bond holders realize all of their interest payments, in full, and get back the entirety of their principal

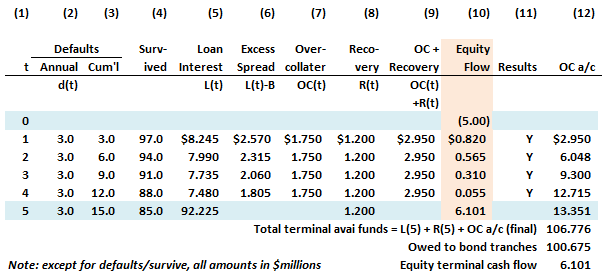

313.3. The following structure is identical to Malz's three-tier securitization structure, with one difference: the scenario reflects an assumption that the annual default is 3.0%. To remind of Malz structure:

(Source: Allan Malz, Financial Risk Management: Models, History, and Institutions (Hoboken, NJ: John Wiley & Sons, 2011))

Which is nearest to the internal rate of return (IRR) for the equity holders?

a. -33.3%

b. 2.09%

c. 11.44%

d. 56.25%

Answers:

Questions:

313.1. Let's assume the same three-tier securitization structure illustrated by Malz section 9.2 with identical assumptions, for convenience:

- The loans in the collateral pool and the liabilities are assumed to have a maturity of five (5) years

- Assets consist of 100 identical leveraged loans with par value of $1.0 million each, priced at par, paying a fixed 8.5%; i.e., 350 bps over LIBOR flat at 5.0%

- Senior debt (senior bonds) of $85.0 million paying a coupon of LIBOR + 50 bps

- Mezzanine debt (junior bonds) of $10.0 million paying a coupon of LIBOR + 500 bps

- This scenario assumes a default rate of 2.0% per annum

- The money market rate is 5.0%

(Source: Allan Malz, Financial Risk Management: Models, History, and Institutions (Hoboken, NJ: John Wiley & Sons, 2011))

Each of the following is true about this structure EXCEPT for which is not?

a. This structure is paying interest to the bondholders of $5.6750 million in each of the five years plus principal repayment in the fifth (5th) year

b. The annual amount diverted to the overcollateralization account is capped at $1.750 million (must be the case, according to the exhibit)

c. The recovery assumption is 40% (must be the case, according to the exhibit)

d. Recovered funds are flowing each year, immediately as recovered, to the equity holders

313.2. The following structure is identical to the previous (and to Malz's illustration in section 9.2) but with one difference: in this scenario, the default rate has been dramatically increased to 10.0% per annum:

(Source: Allan Malz, Financial Risk Management: Models, History, and Institutions (Hoboken, NJ: John Wiley & Sons, 2011))

Under this high-default scenario, which of the following statements is true?

a. There is never a year in which either the junior or senior bonds are paid their full interest

b. Both bond holders (senior and junior) realize all of their interest payments in the first four years, but neither recover their entire obligation in the fifth year (i.e., shortfall for both bond holders)

c. Junior bond holder suffer interest payment shortfalls and a principal shortfall, but senior bond holders receive all of their interest and experience no principal shortfall

d. Both bond holders realize all of their interest payments, in full, and get back the entirety of their principal

313.3. The following structure is identical to Malz's three-tier securitization structure, with one difference: the scenario reflects an assumption that the annual default is 3.0%. To remind of Malz structure:

- The two bond holder classes have a total par value of $95.0 million = $85.0 million senior + $10.0 million mezzanine

- The initial outlay (cash outflow) of the equity holders is $5.0 million

(Source: Allan Malz, Financial Risk Management: Models, History, and Institutions (Hoboken, NJ: John Wiley & Sons, 2011))

Which is nearest to the internal rate of return (IRR) for the equity holders?

a. -33.3%

b. 2.09%

c. 11.44%

d. 56.25%

Answers: