Learning objectives: Compare and contrast market and funding liquidity and describe factors that have impacted by types of liquidity. Describe the regulatory and non-regulatory factors that have affected liquidity. Describe the link between market and funding liquidity. Examine the links between funding liquidity and capital requirements.

Questions:

702.1. Mr. Dudley's remarks focus on the connection between liquidity and market stability. Each of the following statements is asserted by Mr. Dudley EXCEPT which is not true?

a. Research demonstrates that regulatory capital and liquidity requirements improve market liquidity at least in the Treasury and corporate bond markets

b. Market liquidity is the cost (in time and expense) to buy or sell an asset for cash; funding liquidity is the ability of an entity to raise cash by secured or unsecured borrowing

c. Market and funding liquidity are interlinked, especially by way of a negative feedback dynamic during a crisis when market stress impacts funding liquidity which in turn impacts market liquidity

d. The evidence is mixed that market liquidity has diminished in recent years: bid-ask spreads have been been stable (or narrower in the case of corporate bonds), however indirect and anecdotal evidence does suggest a decline in market liquidity

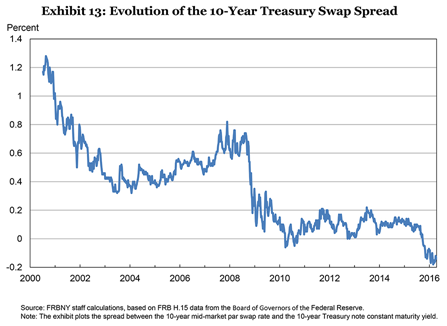

702.2. As vividly illustrated by Dudley's Exhibit 13 (see below) the 10-year swap spread has gradually declined, and actually went into negative territory as of September 2015. The 10-year swap spread is the difference between the fixed-rate paid on a 10-year interest rate swap and the secondary market yield on a 10-year Treasury note. Historically this spread has been naturally positive: an interest rate swap has more credit risk than a Treasury security.

According to Dudley, which of the following is the MOST LIKELY explanation for the unusual shift into a a persistent and negative 10-year Treasury swap spread?

a. Increased supply of U.S. Treasuries

b. More corporations enter swap market as fixed rate payers

c. Too many hedge funds entered the market and "over arbitraged" the spread away

d. Supplementary leverage ratio (SLR) rendered the economics of repo financing less attractive

702.3. Dudley argues that funding liquidity risk can be reduced in four ways. Each of the following is one of these approaches to mitigating funding liquidity risk EXCEPT which is not?

a. Improved transparency and reporting can reduce firms' vulnerability to runs

b. Increased liquidity requirements can reduce to risk of some firms engaging in fire sales

c. Restricting the lender-of-last resort (LOLR) capability according to Dodd-Frank will reduce systematic risk created by procyclicality

d. Funding liquidity is interlined with capital requirements because capital requirements can reduce the risk that a firm becomes insolvent

Answers here:

Questions:

702.1. Mr. Dudley's remarks focus on the connection between liquidity and market stability. Each of the following statements is asserted by Mr. Dudley EXCEPT which is not true?

a. Research demonstrates that regulatory capital and liquidity requirements improve market liquidity at least in the Treasury and corporate bond markets

b. Market liquidity is the cost (in time and expense) to buy or sell an asset for cash; funding liquidity is the ability of an entity to raise cash by secured or unsecured borrowing

c. Market and funding liquidity are interlinked, especially by way of a negative feedback dynamic during a crisis when market stress impacts funding liquidity which in turn impacts market liquidity

d. The evidence is mixed that market liquidity has diminished in recent years: bid-ask spreads have been been stable (or narrower in the case of corporate bonds), however indirect and anecdotal evidence does suggest a decline in market liquidity

702.2. As vividly illustrated by Dudley's Exhibit 13 (see below) the 10-year swap spread has gradually declined, and actually went into negative territory as of September 2015. The 10-year swap spread is the difference between the fixed-rate paid on a 10-year interest rate swap and the secondary market yield on a 10-year Treasury note. Historically this spread has been naturally positive: an interest rate swap has more credit risk than a Treasury security.

According to Dudley, which of the following is the MOST LIKELY explanation for the unusual shift into a a persistent and negative 10-year Treasury swap spread?

a. Increased supply of U.S. Treasuries

b. More corporations enter swap market as fixed rate payers

c. Too many hedge funds entered the market and "over arbitraged" the spread away

d. Supplementary leverage ratio (SLR) rendered the economics of repo financing less attractive

702.3. Dudley argues that funding liquidity risk can be reduced in four ways. Each of the following is one of these approaches to mitigating funding liquidity risk EXCEPT which is not?

a. Improved transparency and reporting can reduce firms' vulnerability to runs

b. Increased liquidity requirements can reduce to risk of some firms engaging in fire sales

c. Restricting the lender-of-last resort (LOLR) capability according to Dodd-Frank will reduce systematic risk created by procyclicality

d. Funding liquidity is interlined with capital requirements because capital requirements can reduce the risk that a firm becomes insolvent

Answers here: