Can you confirm that this is the question that you are referring to in the video? Knowing exactly which question saves us time and helps us to make sure we are responding to you with the correct information.

With reference to the 1st video review for this topic and the question discussed at 3 minutes 40 seconds. Can you please clarify how we got the 95% confidence level and the correlation. These appear to be inputs in the worksheet yet the have not been provided in the question itself. Thanks

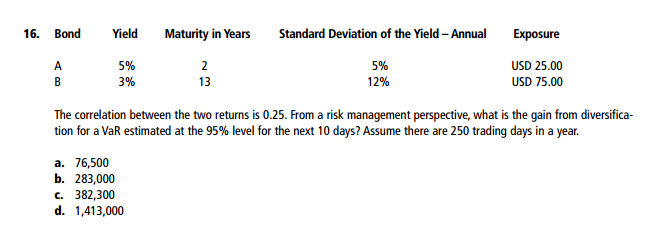

It's my fault, sorry, I totally omitted the actual question from the practice exam (see below) which is "The correlation between the two returns is 0.25. From a risk management perspective, what is the gain from diversification for a VaR estimated at the 95% level for the next 10 days? Assume there are 250 trading days in a year." BTW, the XLS above does solve this; e.g., with correlation = 0, instead, diversified 10-VaR = 37.93

This site uses cookies to help personalise content, tailor your experience and to keep you logged in if you register.

By continuing to use this site, you are consenting to our use of cookies.