Hi David,

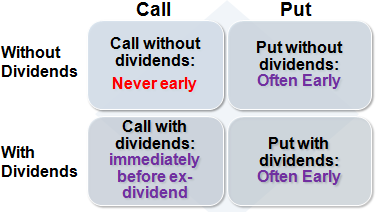

Q1 Put call parity - Practice question (Par 4 difficulty). If the options are instead American-style (paying dividends), when is it optimal to exercise?

- Is it same for both put and call options (i.e before stock goes ex dividend). Because after dividend, stock price should go down and put option holder should exercise after that as S < X and value of put option will increase. Pls suggest.

Q2 If the stock pays a dividend of 2%, how do we adjust the Black-Scholes-Merton to account for the dividends? What is the intuition?

- Can we incorporate this in the BS formula itself like - N(d1) = (log (s/x)+ ( Rf - d + var/2)*t)/vol*sqrt(t) .. Here d is the dividend yield. Although the result is different from N(d1)* exp(-d *t). Infact, when I look your excel sheet given in the solution of Option Gamma - Practice Question (Par 4 difficulty)..you have used the former approach in the formula although dividend there is zero.

Also, in case of N(d1)* exp(-d *t), how to incorporate this for N(d2)? .. look for your guidance.

Thnks

OM

Q1 Put call parity - Practice question (Par 4 difficulty). If the options are instead American-style (paying dividends), when is it optimal to exercise?

- Is it same for both put and call options (i.e before stock goes ex dividend). Because after dividend, stock price should go down and put option holder should exercise after that as S < X and value of put option will increase. Pls suggest.

Q2 If the stock pays a dividend of 2%, how do we adjust the Black-Scholes-Merton to account for the dividends? What is the intuition?

- Can we incorporate this in the BS formula itself like - N(d1) = (log (s/x)+ ( Rf - d + var/2)*t)/vol*sqrt(t) .. Here d is the dividend yield. Although the result is different from N(d1)* exp(-d *t). Infact, when I look your excel sheet given in the solution of Option Gamma - Practice Question (Par 4 difficulty)..you have used the former approach in the formula although dividend there is zero.

Also, in case of N(d1)* exp(-d *t), how to incorporate this for N(d2)? .. look for your guidance.

Thnks

OM

{kind=link}