Hi David,

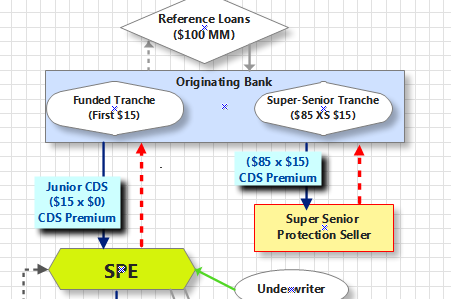

Is the CDO's SPE the CDS protection seller of the unfunded portion of the reference portfolio corresponding to the Super-senior tranche? I am asking because accoring to your sceencast, it seems the protection seller is a different entity.. The Super-senior tranche is one of the CDO tranches, rather than within the reference portfolio, right? Also is it true that the holder (buyer) of the Super-senior tranche indirectly become the protection seller through SPE, because the holder does not pay for Super-senior tranche but receeives CDS payments? In that case, SPE has not risk..

For the regulatory capital calcalation, you said "if left unfunded on balance sheet, assets receive normal risk weight", I wonder what the alternative is? do you mean that if the assets are hedged via CDS, they are not on balance sheet?

Thanks.

Is the CDO's SPE the CDS protection seller of the unfunded portion of the reference portfolio corresponding to the Super-senior tranche? I am asking because accoring to your sceencast, it seems the protection seller is a different entity.. The Super-senior tranche is one of the CDO tranches, rather than within the reference portfolio, right? Also is it true that the holder (buyer) of the Super-senior tranche indirectly become the protection seller through SPE, because the holder does not pay for Super-senior tranche but receeives CDS payments? In that case, SPE has not risk..

For the regulatory capital calcalation, you said "if left unfunded on balance sheet, assets receive normal risk weight", I wonder what the alternative is? do you mean that if the assets are hedged via CDS, they are not on balance sheet?

Thanks.

")

{kind=link}