Hi David,

1. Is the estimate of correlation provided by regulator under Advanced IRB?

2. Does IRB also account for Credit Risk Migration (CRM)?

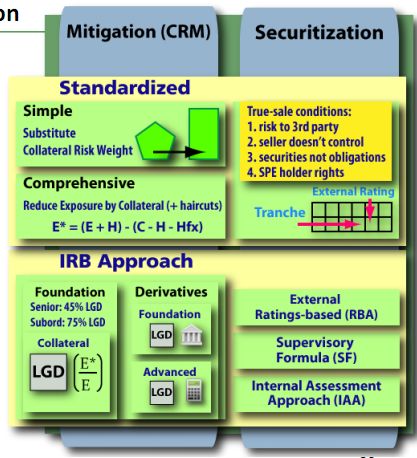

3. What is the purpose of Ratings-Based Approach (RBA), Supervisory Formula (SF), and Internal Assessment Approach (IAA)? Are they for the treatment of securitisation exposures?

many thanks!

1. Is the estimate of correlation provided by regulator under Advanced IRB?

2. Does IRB also account for Credit Risk Migration (CRM)?

3. What is the purpose of Ratings-Based Approach (RBA), Supervisory Formula (SF), and Internal Assessment Approach (IAA)? Are they for the treatment of securitisation exposures?

many thanks!

")

{kind=link}