You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

capital ratio

- Thread starter ajsa

- Start date

Hi asja,

1. Capital itself is not identified/parsed as credit-vs-market-vs-ops capital, so it is nearer to "as long as the total capital divided by the total RWA is at least 8%, then it is fine?" but not quite. Because: total capital / (credit risk + market risk + ops risk) > 8% (x scaling factor, I think it's still 1.06) ... you can see it's like a "pool" of capital against the total risk-adjusted asset equivalent...

...note #1: the distinction that does matter is Tier I (core), II (supplemental)) & III capital. There are conditions on these. But these are categories that distinguish the quality of the capital buffer itself, not the firm's risk. You might think of this in terms of balance sheet:

* capital is right-hand side, like equity (although not book equity)

* risk is generally a feature of the left-hand side assets (e.g., market risk is the risk the assets will drop in value)

...caveat #2: Tier 3 is for market risk only

so this basel capital adaquacy ratio: capital / risk-weighted assets ... is a complex variation on (i.e., adjustments), but "structurally" similar to:

plain old leverage ratio = equity / assets

(the question here was "what does it mean that PD is a decreasing function?")

2. this refers to (advanced) credit risk IRB charge:

if you like, here is last year's spreadsheet:

http://www.bionicturtle.com/premium/spreadsheet/2008_oprisk_basel_ii_internal_ratings_based_irb/

(I will be improving on new one soon; I will add the PD curve...)

http://learn.bionicturtle.com/images/forum/0919_irb.png

the correlation is actually used here as in a Gaussian copula (see Hull 22), it is Greek rho above. This use of correlation was controversial before the crisis, even more so now. If you want an loose analogy, it is rather like beta in CAPM; i.e., "single factor" in ASFR model. I highly recommend reading the 19 page assignment on IRB risk weight function, here is what it says on the correlation:

"The single systematic risk factor needed in the ASRF model may be interpreted as reflecting the state of the global economy. The degree of the obligor’s exposure to the systematic risk factor is expressed by the asset correlation. The asset correlations, in short, show how the asset value (e.g. sum of all asset values of a firm) of one borrower depends on the asset value of another borrower. Likewise, the correlations could be described as the dependence of the asset value of a borrower on the general state of the economy - all borrowers are linked to each other by this single risk factor."

put another way, correlation is to an (abstract) single factor, and this is a way of varying the impact of the asset type on the credit portfolio; lower rho for assets with higher idiosyncratic risk, higher rho for assets with higher systemic risk.

Question to ponder (for you): how does this IRB account for assets with high systemic risk and what is the impact on capital charge?

The "diminishing effect of PD" could have two meanings (PD is inside the maturity term, which is complicated) but surely means: in the IRB above, PD is not linear on the capital charge (it's concave; i.e., the 1st derivative is decreasing)

David

1. Capital itself is not identified/parsed as credit-vs-market-vs-ops capital, so it is nearer to "as long as the total capital divided by the total RWA is at least 8%, then it is fine?" but not quite. Because: total capital / (credit risk + market risk + ops risk) > 8% (x scaling factor, I think it's still 1.06) ... you can see it's like a "pool" of capital against the total risk-adjusted asset equivalent...

...note #1: the distinction that does matter is Tier I (core), II (supplemental)) & III capital. There are conditions on these. But these are categories that distinguish the quality of the capital buffer itself, not the firm's risk. You might think of this in terms of balance sheet:

* capital is right-hand side, like equity (although not book equity)

* risk is generally a feature of the left-hand side assets (e.g., market risk is the risk the assets will drop in value)

...caveat #2: Tier 3 is for market risk only

so this basel capital adaquacy ratio: capital / risk-weighted assets ... is a complex variation on (i.e., adjustments), but "structurally" similar to:

plain old leverage ratio = equity / assets

(the question here was "what does it mean that PD is a decreasing function?")

2. this refers to (advanced) credit risk IRB charge:

if you like, here is last year's spreadsheet:

http://www.bionicturtle.com/premium/spreadsheet/2008_oprisk_basel_ii_internal_ratings_based_irb/

(I will be improving on new one soon; I will add the PD curve...)

http://learn.bionicturtle.com/images/forum/0919_irb.png

{kind=link}

the correlation is actually used here as in a Gaussian copula (see Hull 22), it is Greek rho above. This use of correlation was controversial before the crisis, even more so now. If you want an loose analogy, it is rather like beta in CAPM; i.e., "single factor" in ASFR model. I highly recommend reading the 19 page assignment on IRB risk weight function, here is what it says on the correlation:

"The single systematic risk factor needed in the ASRF model may be interpreted as reflecting the state of the global economy. The degree of the obligor’s exposure to the systematic risk factor is expressed by the asset correlation. The asset correlations, in short, show how the asset value (e.g. sum of all asset values of a firm) of one borrower depends on the asset value of another borrower. Likewise, the correlations could be described as the dependence of the asset value of a borrower on the general state of the economy - all borrowers are linked to each other by this single risk factor."

put another way, correlation is to an (abstract) single factor, and this is a way of varying the impact of the asset type on the credit portfolio; lower rho for assets with higher idiosyncratic risk, higher rho for assets with higher systemic risk.

Question to ponder (for you): how does this IRB account for assets with high systemic risk and what is the impact on capital charge?

The "diminishing effect of PD" could have two meanings (PD is inside the maturity term, which is complicated) but surely means: in the IRB above, PD is not linear on the capital charge (it's concave; i.e., the 1st derivative is decreasing)

David

Hi David,

1. Tier 3 can only be used for market risk. it lead me to think that their is minimum capital requirement for each risk type. Or do I miss anything? (Sorry I am a little lost of your point while reading your answer..)

2. To try to answer your question (for me to ponder), since PD estimate accounts for the correlation, high correlation (high systemic risk?) =>low PD=>low capital charge. Is it correct? Sorry not too sure..")

3, Is capital charge same as capital requirement?

4. where is the the Risk-weight function in IRB's RWa formula?

RWA = 12.5 * K * EAD

K = LGD * f(PD) * f(M, b)

5. BTW, is the 'b' in the above fomula EAD?

Thanks.

1. Tier 3 can only be used for market risk. it lead me to think that their is minimum capital requirement for each risk type. Or do I miss anything? (Sorry I am a little lost of your point while reading your answer..)

2. To try to answer your question (for me to ponder), since PD estimate accounts for the correlation, high correlation (high systemic risk?) =>low PD=>low capital charge. Is it correct? Sorry not too sure..

3, Is capital charge same as capital requirement?

4. where is the the Risk-weight function in IRB's RWa formula?

RWA = 12.5 * K * EAD

K = LGD * f(PD) * f(M, b)

5. BTW, is the 'b' in the above fomula EAD?

Thanks.

Hi asja,

1. Yes, each risk type has a minimum captial requirement, but they roll-up...

Did you see the XLS associated with the tutorial? I had hoped this would be helpful:

http://www.bionicturtle.com/premium/spreadsheet/7.d.1_b2_adequacy/

e.g., if a bank had plenty of Tier 1, it could just meet the sum of credit+market+operational with all Tier 1... the reason the worksheet is "complicated" is due to limits on Tier 2 & Tier 3

so, the restrictions are on the Tier 2 and 3 generally. Actually, being Basel, they have a bunch of rules (e.g., Tier 1 and 2 have upper/lower) but we care about:

* Tier 2 no more than 100% of Tier 1

* Tier 3 for market risk only

2. No but almost, good try! ... higher correlation = high systemic risk implies higher capital charge. One way to think about this is to look at the formula and imagine rho (correlation) of zero; i.e, no systemic risk and all idiosyncratic risk. Basel IRB treats this like an instrument with zero risk and...look inside formula above, if rho = 0:

LGD * N(N-1(PD*1) + N-1(99.9%)*0) - LGD*PD

= LGD * N(N-1(PD*1)) - LGD*PD

since N(N-1(PD)) = PD !!

LGD * PD - LGD*PD = 0

so the formula then is basically increasing the UL as correlation increases (the asset correlations have floors, so this outcome is not possible, it's just how i manage it mentally)

3. I think so ... i use them equivalently ...

4. I don't follow ... the function (K) produces a captial charge, it is converted to risk weighted asset equivalent by multiplying by 12.5 because that is 1/8

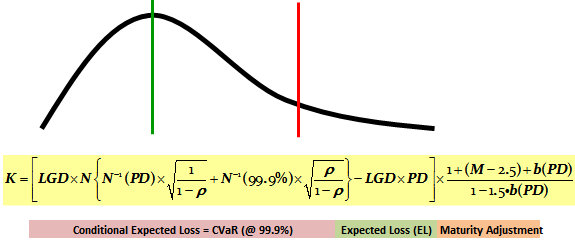

5. No, if you look up at the yellow IRB (K = ), b(.) is a function of PD. So, the maturity function actually incorporates PD...very counterintuive ... de Servigny has an explain but amounts to conservatism

David

1. Yes, each risk type has a minimum captial requirement, but they roll-up...

Did you see the XLS associated with the tutorial? I had hoped this would be helpful:

http://www.bionicturtle.com/premium/spreadsheet/7.d.1_b2_adequacy/

e.g., if a bank had plenty of Tier 1, it could just meet the sum of credit+market+operational with all Tier 1... the reason the worksheet is "complicated" is due to limits on Tier 2 & Tier 3

so, the restrictions are on the Tier 2 and 3 generally. Actually, being Basel, they have a bunch of rules (e.g., Tier 1 and 2 have upper/lower) but we care about:

* Tier 2 no more than 100% of Tier 1

* Tier 3 for market risk only

2. No but almost, good try! ... higher correlation = high systemic risk implies higher capital charge. One way to think about this is to look at the formula and imagine rho (correlation) of zero; i.e, no systemic risk and all idiosyncratic risk. Basel IRB treats this like an instrument with zero risk and...look inside formula above, if rho = 0:

LGD * N(N-1(PD*1) + N-1(99.9%)*0) - LGD*PD

= LGD * N(N-1(PD*1)) - LGD*PD

since N(N-1(PD)) = PD !!

LGD * PD - LGD*PD = 0

so the formula then is basically increasing the UL as correlation increases (the asset correlations have floors, so this outcome is not possible, it's just how i manage it mentally)

3. I think so ... i use them equivalently ...

4. I don't follow ... the function (K) produces a captial charge, it is converted to risk weighted asset equivalent by multiplying by 12.5 because that is 1/8

5. No, if you look up at the yellow IRB (K = ), b(.) is a function of PD. So, the maturity function actually incorporates PD...very counterintuive ... de Servigny has an explain but amounts to conservatism

David

Hi David,

1. For 7.d.1_b2_adequacy spreadsheet, I wonder how tier1 and tier3 capital are allocated for market risk since both have extra? ie, why not tier3=350 and tier1=0 so the totally will be 1,650 than 1,550, and so it will end up with a higher capital ratio for the bank?

2. OK.. I thought high correlation would lead to low PD as shown here.

http://forum.bionicturtle.com/viewthread/1815/

But it seems low PD does not mean low K, and K=LGD*PD*f(M,b) is misleading, right?

4. So I think K is the risk weighing function, right? I was confused because K is called "capital requirement", but I think K*EAD should be called capital requirement or capital charge, and RWA = capital requirement * 12.5. Please let me know if you disagree.

Thanks.

1. For 7.d.1_b2_adequacy spreadsheet, I wonder how tier1 and tier3 capital are allocated for market risk since both have extra? ie, why not tier3=350 and tier1=0 so the totally will be 1,650 than 1,550, and so it will end up with a higher capital ratio for the bank?

2. OK.. I thought high correlation would lead to low PD as shown here.

http://forum.bionicturtle.com/viewthread/1815/

But it seems low PD does not mean low K, and K=LGD*PD*f(M,b) is misleading, right?

4. So I think K is the risk weighing function, right? I was confused because K is called "capital requirement", but I think K*EAD should be called capital requirement or capital charge, and RWA = capital requirement * 12.5. Please let me know if you disagree.

Thanks.

Hi asja,

1. See note in cell M15: "<< Tier 3 limited to market risk and not > 250% of Tier 1. The rest is not eligible"

so if the capital charge for market risk = $350, $250 is the most Tier 3 that can be used:

T1 + 2.5*T1 = 350

3.5T1 = 350, T1 = 100

2.

Re: "high correlation would lead to low PD as shown here."

That's in regard to *default correlation* for the junior tranche;

for the senior tranche, high correlation leads to higher PD

...so please note this refers to different types of dependence

...however, the connection is profound in a way: the senior tranche is most exposed to *systemic risk*

...so metaphorically only, i think it's safe to "liken" the asset here to a senior tranche but better to just focus on the formula

K=LGD*PD*f(M,b) is misleading, right?

this formula is from de Servigny. It is stylized (abstract) but I see your point: strictly speaking, it can be misleading if taken literally...i think maybe i will remove going forward...good point

4. I do see your point and I do agree with you! take an example:

$1 MM exposure = EAD

K = f[pd, lgd, m] = 1%; that is Basel's usage from the IRB document

but capital requirement or capital capital = K * EAD = 1% * $1 MM = $10,000

RWA = 10,000 * 12.5 = 125,000

(simply so that by definition 8% of 125,000 = $10,000)

kudos for your precision on that..OH, MAYBE you have "discovered" this difference btwn capital requirement and capital charge? maybe K = requirement and K*EAD = charge? ... I'll let you know if i find out

Thanks, David

1. See note in cell M15: "<< Tier 3 limited to market risk and not > 250% of Tier 1. The rest is not eligible"

so if the capital charge for market risk = $350, $250 is the most Tier 3 that can be used:

T1 + 2.5*T1 = 350

3.5T1 = 350, T1 = 100

2.

Re: "high correlation would lead to low PD as shown here."

That's in regard to *default correlation* for the junior tranche;

for the senior tranche, high correlation leads to higher PD

...so please note this refers to different types of dependence

...however, the connection is profound in a way: the senior tranche is most exposed to *systemic risk*

...so metaphorically only, i think it's safe to "liken" the asset here to a senior tranche but better to just focus on the formula

K=LGD*PD*f(M,b) is misleading, right?

this formula is from de Servigny. It is stylized (abstract) but I see your point: strictly speaking, it can be misleading if taken literally...i think maybe i will remove going forward...good point

4. I do see your point and I do agree with you! take an example:

$1 MM exposure = EAD

K = f[pd, lgd, m] = 1%; that is Basel's usage from the IRB document

but capital requirement or capital capital = K * EAD = 1% * $1 MM = $10,000

RWA = 10,000 * 12.5 = 125,000

(simply so that by definition 8% of 125,000 = $10,000)

kudos for your precision on that..OH, MAYBE you have "discovered" this difference btwn capital requirement and capital charge? maybe K = requirement and K*EAD = charge? ... I'll let you know if i find out

Thanks, David

Hi David,

2. for K=LGD*PD*f(M,b), I am not sure if it is a different (or simplified) approach from ASRF, or it is just not strict. Could you pls confirm? In the exam, does it mean I am not supposed to use K=LGD*PD*f(M,b)?

4. sorry one more thing. Is the K risk weighing function? I do not see how it "weighs" based on different rating/exposure type like what happens in the standard approach. Maybe it is just a single factor, and it weighs on the whole EAD?

Thanks again.

2. for K=LGD*PD*f(M,b), I am not sure if it is a different (or simplified) approach from ASRF, or it is just not strict. Could you pls confirm? In the exam, does it mean I am not supposed to use K=LGD*PD*f(M,b)?

4. sorry one more thing. Is the K risk weighing function? I do not see how it "weighs" based on different rating/exposure type like what happens in the standard approach. Maybe it is just a single factor, and it weighs on the whole EAD?

Thanks again.

Hi asja,

2. K=LGD*PD*f(M,b) is from de Servigny (p 402). It is defintely "stylized" version of the above (correct) IRB. ASRF is the underlying "framework" that contains the set of (unrealistic) assumptions that, if accepted, justify the IRB risk weight function above. Re: "I am not supposed to use K=LGD*PD*f(M,b)?" It can't be used "as is:" it is just a way to list the components and show IRB uses a function (rather than the loookup table of standardized)

4. I take "weight" to be a metaphor. The function gives greater "weight " to greater risk by producing higher values for assets with higher correlations (to systemic risk factor), longer maturities, higher conditional PDs ... unlike the standardized lookup table, it's a function

David

2. K=LGD*PD*f(M,b) is from de Servigny (p 402). It is defintely "stylized" version of the above (correct) IRB. ASRF is the underlying "framework" that contains the set of (unrealistic) assumptions that, if accepted, justify the IRB risk weight function above. Re: "I am not supposed to use K=LGD*PD*f(M,b)?" It can't be used "as is:" it is just a way to list the components and show IRB uses a function (rather than the loookup table of standardized)

4. I take "weight" to be a metaphor. The function gives greater "weight " to greater risk by producing higher values for assets with higher correlations (to systemic risk factor), longer maturities, higher conditional PDs ... unlike the standardized lookup table, it's a function

David

Hi David,

2. "higher correlation = high systemic risk implies higher capital charge. One way to think about this is to look at the formula and imagine rho (correlation) of zero; i.e, no systemic risk and all idiosyncratic risk. Basel IRB treats this like an instrument with zero risk and…look inside formula above, if rho = 0:

LGD * N(N-1(PD*1) + N-1(99.9%)*0) - LGD*PD

= LGD * N(N-1(PD*1)) - LGD*PD

since N(N-1(PD)) = PD !!

LGD * PD - LGD*PD = 0

so the formula then is basically increasing the UL as correlation increases"

But It seems to me high correlation only increases the UL than PD.. Also Schweser says "correlation decreases with high PD and high PD suggests more idiosyncratic risk".. Sorry still a little confused..

Thanks.

2. "higher correlation = high systemic risk implies higher capital charge. One way to think about this is to look at the formula and imagine rho (correlation) of zero; i.e, no systemic risk and all idiosyncratic risk. Basel IRB treats this like an instrument with zero risk and…look inside formula above, if rho = 0:

LGD * N(N-1(PD*1) + N-1(99.9%)*0) - LGD*PD

= LGD * N(N-1(PD*1)) - LGD*PD

since N(N-1(PD)) = PD !!

LGD * PD - LGD*PD = 0

so the formula then is basically increasing the UL as correlation increases"

But It seems to me high correlation only increases the UL than PD.. Also Schweser says "correlation decreases with high PD and high PD suggests more idiosyncratic risk".. Sorry still a little confused..

Thanks.

Hi asja

Right, both statements are correct and consistent:

"But It seems to me high correlation only increases the UL than PD."

That's correct, the conditional expected loss - EL = effectively the UL

higher correlation (rho) is increaseing the conditional EL term above; if rho = 0, CEL = EL, and UL = 0

Also Schweser says “correlation decreases with high PD and high PD suggests more idiosyncratic risk”.. That's correct, too, but it refers their relationship as two inputs into the formula

e.g., corporate use rho of 12 - 24% but nearer to 24% if the PD is low

(but this is non-essential and, I think, impossible to comprehend without fundamentals. I would not try to get this directly w/o first meditating on the IRB function...this is "merely" about calibrating inputs...i would step back first)

David

Right, both statements are correct and consistent:

"But It seems to me high correlation only increases the UL than PD."

That's correct, the conditional expected loss - EL = effectively the UL

higher correlation (rho) is increaseing the conditional EL term above; if rho = 0, CEL = EL, and UL = 0

Also Schweser says “correlation decreases with high PD and high PD suggests more idiosyncratic risk”.. That's correct, too, but it refers their relationship as two inputs into the formula

e.g., corporate use rho of 12 - 24% but nearer to 24% if the PD is low

(but this is non-essential and, I think, impossible to comprehend without fundamentals. I would not try to get this directly w/o first meditating on the IRB function...this is "merely" about calibrating inputs...i would step back first)

David

....In case we get lost in detail, here is my opinion on what we essentially care about (in regard to this IRB):

Conditional EL - EL = UL is the basis for the capital charge

(Conditional EL = conditonal PD * downturn LGD;

i.e., the EL is "transformed" into a "worser case" EL in order to achieve a UL. If this part is puzzling, congratulations, you join a club of folks who find this to be a bit of sleight of hand! a cheat even!)

so the Conditional EL is the key calculation and depend on, in addition to PD, (see the two terms):

1. 99.9% confidence

2. asset correlation (rho) to the "single factor" (systemic); i.e., higher correlation = higher CEL = higher risk charge

if you look at CEL above, rho is weighting the relative importance of 99.9% and asset PD

(a customer last year likened the ASRF rho to beta in CAPM. But, okay, just a metaphor, but I like it! Both are single factor models! higher beta like higher rho implies higher system risk and, respectively, greater return or credit risk and lower idiosyncratic risk. And idiosyncratic risk does not make an appearance, it does not count, it is assumed to disappear into the "well-diversified [i.e., portfolio invariance]" portfolo...so CAPM is a nice way into the credit ASRF )

David

Conditional EL - EL = UL is the basis for the capital charge

(Conditional EL = conditonal PD * downturn LGD;

i.e., the EL is "transformed" into a "worser case" EL in order to achieve a UL. If this part is puzzling, congratulations, you join a club of folks who find this to be a bit of sleight of hand! a cheat even!)

so the Conditional EL is the key calculation and depend on, in addition to PD, (see the two terms):

1. 99.9% confidence

2. asset correlation (rho) to the "single factor" (systemic); i.e., higher correlation = higher CEL = higher risk charge

if you look at CEL above, rho is weighting the relative importance of 99.9% and asset PD

(a customer last year likened the ASRF rho to beta in CAPM. But, okay, just a metaphor, but I like it! Both are single factor models! higher beta like higher rho implies higher system risk and, respectively, greater return or credit risk and lower idiosyncratic risk. And idiosyncratic risk does not make an appearance, it does not count, it is assumed to disappear into the "well-diversified [i.e., portfolio invariance]" portfolo...so CAPM is a nice way into the credit ASRF )

David

Now that, I haven't thought about.. I don't think I've read anything about diversification yet, but I know AMA does take into account correlation effects.. so that's something I'd want to know too!

Just a thought, I don't know if it's okay to leave personal info. on here, but I'm wondering ajsa, if you are interested in exchanging e-mails or instant messenger nicknames so we can review the FRM exam together. I've talked to David a while ago about maybe opening up an online chat room where candidates can discuss about FRM topics instantly online..

so if you are interested, here is my info.

.(JavaScript must be enabled to view this email address)

msn: .(JavaScript must be enabled to view this email address)

or if you'd prefer other messengers, I'd be glad to set it up.

I'm not sure if leaving this info in the post is allowed, sorry if it's not and I will delete this upon notice!

Thanks.

Just a thought, I don't know if it's okay to leave personal info. on here, but I'm wondering ajsa, if you are interested in exchanging e-mails or instant messenger nicknames so we can review the FRM exam together. I've talked to David a while ago about maybe opening up an online chat room where candidates can discuss about FRM topics instantly online..

so if you are interested, here is my info.

.(JavaScript must be enabled to view this email address)

msn: .(JavaScript must be enabled to view this email address)

or if you'd prefer other messengers, I'd be glad to set it up.

I'm not sure if leaving this info in the post is allowed, sorry if it's not and I will delete this upon notice!

Thanks.

Hi asja,

I think Jack's point about "porfolio invariance" is good and relevant: under the ASRF, IRB assumes the credit portfolio is diversified (granular) and therefore does not explicitly factor idiosyncratic risk; i.e., the statement "IRB does not incorporate the risk-reducing role of diversification," IMO, is incorrect: IRB, by definition, assuming *idiosyncratic credit* risk is diversified away.

if we think about the risk of an obligor:

risk = systemic + idiosyncratic

idiosyncratic risk: ASRF via portfolio invariance, assumes idiosyncratic risk = 0 (how can this be? Supervisors are expected to treat realistic "undiversified" portfolios via Pillar 2)

Systemic risk: that's determined in the IRB function which includes correlation. The correlation in IRB is used to calibrate the systemic risk (exposure to the same macroeconomic factor) ... A higher correlation in IRB implies a higher correlation to the (abstract) "single systematic risk factor." ... I like to understand this by imagining rho = 0 in the IRB (which it can never be, it has floors). Then the IRB above reduces to 0! i.e., no systemic risk and (per invariance) no idiosyncratic risk (!!)

i realize the rho contributing to systemic risk is counter-intuitive. That's why i referred to CAPM as an analogy:

E(return) = beta * ERP + etc....

here the beta is the measure of systemic risk (sensitivity to market)... but recall beta is just a translated correlation:

beta = covariance ()/variance = correlation * volatility/volatility = correlation * cross-volatility

(I would totally seperate out Basel OpRisk AMA from this topic...i don't see how it relates)

@Jack: thanks for asking about leaving contact info. That's fine by me ... I am thinking about adding instant chat for the next site version ...

David

I think Jack's point about "porfolio invariance" is good and relevant: under the ASRF, IRB assumes the credit portfolio is diversified (granular) and therefore does not explicitly factor idiosyncratic risk; i.e., the statement "IRB does not incorporate the risk-reducing role of diversification," IMO, is incorrect: IRB, by definition, assuming *idiosyncratic credit* risk is diversified away.

if we think about the risk of an obligor:

risk = systemic + idiosyncratic

idiosyncratic risk: ASRF via portfolio invariance, assumes idiosyncratic risk = 0 (how can this be? Supervisors are expected to treat realistic "undiversified" portfolios via Pillar 2)

Systemic risk: that's determined in the IRB function which includes correlation. The correlation in IRB is used to calibrate the systemic risk (exposure to the same macroeconomic factor) ... A higher correlation in IRB implies a higher correlation to the (abstract) "single systematic risk factor." ... I like to understand this by imagining rho = 0 in the IRB (which it can never be, it has floors). Then the IRB above reduces to 0! i.e., no systemic risk and (per invariance) no idiosyncratic risk (!!)

i realize the rho contributing to systemic risk is counter-intuitive. That's why i referred to CAPM as an analogy:

E(return) = beta * ERP + etc....

here the beta is the measure of systemic risk (sensitivity to market)... but recall beta is just a translated correlation:

beta = covariance ()/variance = correlation * volatility/volatility = correlation * cross-volatility

(I would totally seperate out Basel OpRisk AMA from this topic...i don't see how it relates)

@Jack: thanks for asking about leaving contact info. That's fine by me ... I am thinking about adding instant chat for the next site version ...

David

Hi David,

Sorry for any of my confusions.. I understand that IRB just "assumes" diversification, but leave regulator to adjust risk weight for idiosyncratic risks. Does not it that mean ” IRB does not incorporate the risk-reducing role of diversification”?

Also for “porfolio invariance”, "The model should be portfolio invariant, i.e. the capital required for any given loan should

only depend on the risk of that loan and must not depend on the portfolio it is added to."

It also looks like that ASRF does not consider diversification effect..

Thanks.

Sorry for any of my confusions.. I understand that IRB just "assumes" diversification, but leave regulator to adjust risk weight for idiosyncratic risks. Does not it that mean ” IRB does not incorporate the risk-reducing role of diversification”?

Also for “porfolio invariance”, "The model should be portfolio invariant, i.e. the capital required for any given loan should

only depend on the risk of that loan and must not depend on the portfolio it is added to."

It also looks like that ASRF does not consider diversification effect..

Thanks.

Hi asja,

Oh, okay, I think I see your point ... and note just after the sentence you quote, the IRB document says:

"The desire for portfolio invariance, however, makes recognition of institution-specific diversification effects within the framework difficult: diversification effects would depend on how well a new loan fits into an existing portfolio."

...which seems to support the statement

but, really, this just speaks to the imprecision of the statement: "IRB does not incorporate the risk-reducing role of diversification"

I can say, on the one hand, as i did above: false: by not counting idiosyncratic risk and assuming portfolio invariance, IRB gives full credit for benefits of diversification;

or we can say, per your aguments: true: IRB does not give insititution-specifid diversification benefits

and, finally, there is the issue of pillar 2 supervisory override, which is not IRB but does allow the supervisor to adjust for concentration (i.e., the lack of diversification)

...so I do see your point, I revise to suggest this depends on the how you interpret the question

David

Oh, okay, I think I see your point ... and note just after the sentence you quote, the IRB document says:

"The desire for portfolio invariance, however, makes recognition of institution-specific diversification effects within the framework difficult: diversification effects would depend on how well a new loan fits into an existing portfolio."

...which seems to support the statement

but, really, this just speaks to the imprecision of the statement: "IRB does not incorporate the risk-reducing role of diversification"

I can say, on the one hand, as i did above: false: by not counting idiosyncratic risk and assuming portfolio invariance, IRB gives full credit for benefits of diversification;

or we can say, per your aguments: true: IRB does not give insititution-specifid diversification benefits

and, finally, there is the issue of pillar 2 supervisory override, which is not IRB but does allow the supervisor to adjust for concentration (i.e., the lack of diversification)

...so I do see your point, I revise to suggest this depends on the how you interpret the question

David

Hello David,

I think I have a firm grasp on the - higher systematic risk = higher capital charge concept (higher rho = higher charge), but as you mentioned,

“correlation decreases with high PD and high PD suggests more idiosyncratic risk”.. That’s correct, too, but it refers their relationship as two inputs into the formula

e.g., corporate use rho of 12 - 24% but nearer to 24% if the PD is low.

I think I have trouble incorporating this idea above with "higher systematic risk = higher capital charge", since higher systematic risk refers to lower PD, and lower PD would suggest less capital requirement right? (They seem conflicting)

I understand maybe these are two separate ideas, but I'm having trouble connecting the two..

I read the explanatory note and I it says "asset correlations decrease with increasing PDs... the higher the PD, the higher the idiosyncratic risk components of a borrower. The default risk depends less on the overall state of the economy and more on individual risk drivers."

so as you said, "corporate use rho of 12 - 24% but nearer to 24% if the PD is low", in that case, a firm would actually be subjected to higher capital requirement (higher rho) when their PD is low? or maybe it is due to the fact that it is holding more capital that is making its PD lower?

I really need your guidance with this, and would really appreciate your help!

Thank you.

I think I have a firm grasp on the - higher systematic risk = higher capital charge concept (higher rho = higher charge), but as you mentioned,

“correlation decreases with high PD and high PD suggests more idiosyncratic risk”.. That’s correct, too, but it refers their relationship as two inputs into the formula

e.g., corporate use rho of 12 - 24% but nearer to 24% if the PD is low.

I think I have trouble incorporating this idea above with "higher systematic risk = higher capital charge", since higher systematic risk refers to lower PD, and lower PD would suggest less capital requirement right? (They seem conflicting)

I understand maybe these are two separate ideas, but I'm having trouble connecting the two..

I read the explanatory note and I it says "asset correlations decrease with increasing PDs... the higher the PD, the higher the idiosyncratic risk components of a borrower. The default risk depends less on the overall state of the economy and more on individual risk drivers."

so as you said, "corporate use rho of 12 - 24% but nearer to 24% if the PD is low", in that case, a firm would actually be subjected to higher capital requirement (higher rho) when their PD is low? or maybe it is due to the fact that it is holding more capital that is making its PD lower?

I really need your guidance with this, and would really appreciate your help!

Thank you.

Hi Jack - Right, understood, it's a very *perceptive* observation.

Starting with the IRB capital charge: K = f[PD, LGD, EAD, M, rho]

in regard to this IRB formula, higher PD implies higher K

(you can verify with IRB formula @ http://www.bionicturtle.com/premium/spreadsheet/7.d.3_b2_credit_irb/)

so at the level of the IRB formula, greater risk of default implies greater charge.

also in regard to the IRB formula, higher rho signifies greater exposure to systematic risk (ASRF). Higher rho here, just as you say, is: higher systematic risk = higher capital charge concept (higher rho = higher charge)

Now move to the "second order" issue (or precursor question): what rho must be used as an input into this IRB formula?

No choice: Basel ruleset says the rho is function of (i) exposure type and (ii) PD

...and in regard to the *calibration of rho as input,* lower PD implies higher rho (on the theory that lower PD associates with more systemic and less idiosyncratic risk).

so, for example, let's assume a high-quality (i.e., highly rated, low PD) corporate exposure:

1. the rho input will be nearer to 24% than 12%; i.e., higher rho due to low PD reflecting presumption of higher systemic risk

2. In regard to the IRB formula, the lower PD (per se) will lower the charge but the higher rho has the opposite impact

let me carry this "contradiction further:" the (M) is 2.5 under foundation IRB but uses a formula under advanced IRB. In the maturity adjustment, lower PD creates a higher maturity adjustment (huh?), which is terribly confusing. But you can see the similarity? In effect, for advanced IRB:

* a high-quality (low PD) exposure will, of course, benefit from the "first-order" reduction in capital charge due to the lower PD

* HOWEVER, under advanced IRB, both (rho) and (M) will be increased due precisely to this low PD. And this will offset the lower charge (thought prob not entirely)!

each of these "mitigants" has a formal explain, but I prefer to think of simply as "conversative buffer:" your low PD earns you a low charge, but we aren't taking chances, we are going to mitigate the benefit

Now that i've tried to explain, it occurs to me that the confusion seems to arise (correct me if you disagree?) because Basel uses PD three times: once where we expect (PD*LGD) but twice where it unexpectedly "infects" the IRB, in rho and (M), which is counterintuive.

Hope that helps...David

Starting with the IRB capital charge: K = f[PD, LGD, EAD, M, rho]

in regard to this IRB formula, higher PD implies higher K

(you can verify with IRB formula @ http://www.bionicturtle.com/premium/spreadsheet/7.d.3_b2_credit_irb/)

so at the level of the IRB formula, greater risk of default implies greater charge.

also in regard to the IRB formula, higher rho signifies greater exposure to systematic risk (ASRF). Higher rho here, just as you say, is: higher systematic risk = higher capital charge concept (higher rho = higher charge)

Now move to the "second order" issue (or precursor question): what rho must be used as an input into this IRB formula?

No choice: Basel ruleset says the rho is function of (i) exposure type and (ii) PD

...and in regard to the *calibration of rho as input,* lower PD implies higher rho (on the theory that lower PD associates with more systemic and less idiosyncratic risk).

so, for example, let's assume a high-quality (i.e., highly rated, low PD) corporate exposure:

1. the rho input will be nearer to 24% than 12%; i.e., higher rho due to low PD reflecting presumption of higher systemic risk

2. In regard to the IRB formula, the lower PD (per se) will lower the charge but the higher rho has the opposite impact

let me carry this "contradiction further:" the (M) is 2.5 under foundation IRB but uses a formula under advanced IRB. In the maturity adjustment, lower PD creates a higher maturity adjustment (huh?), which is terribly confusing. But you can see the similarity? In effect, for advanced IRB:

* a high-quality (low PD) exposure will, of course, benefit from the "first-order" reduction in capital charge due to the lower PD

* HOWEVER, under advanced IRB, both (rho) and (M) will be increased due precisely to this low PD. And this will offset the lower charge (thought prob not entirely)!

each of these "mitigants" has a formal explain, but I prefer to think of simply as "conversative buffer:" your low PD earns you a low charge, but we aren't taking chances, we are going to mitigate the benefit

Now that i've tried to explain, it occurs to me that the confusion seems to arise (correct me if you disagree?) because Basel uses PD three times: once where we expect (PD*LGD) but twice where it unexpectedly "infects" the IRB, in rho and (M), which is counterintuive.

Hope that helps...David

Similar threads

- Replies

- 2

- Views

- 250

- Replies

- 0

- Views

- 276

- Replies

- 0

- Views

- 117

- Replies

- 1

- Views

- 341