Shau_2207

Member

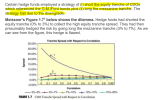

Hello David,

Can you please confirm if the mentioned hedge fund Strategy correct?

I think its flipped,

1) Long Equity Tranche CDO=> Decreased correlation => Spreads widen (instead of expected tighten ie becoming better-off ) => Loose money

2) Short Mezzanine tranche CDO => Decreased correlation => Spreads Tighten ( Instead of expected widen ie becoming worse -off) => Loose money.

Can you please confirm if the mentioned hedge fund Strategy correct?

I think its flipped,

1) Long Equity Tranche CDO=> Decreased correlation => Spreads widen (instead of expected tighten ie becoming better-off ) => Loose money

2) Short Mezzanine tranche CDO => Decreased correlation => Spreads Tighten ( Instead of expected widen ie becoming worse -off) => Loose money.