Hi David,

I am watching your Credit A, Part 1 episode 7....I think I understand the Merton model for valuing the debt of a firm. I've also understood the mechanics of working the associated EditGrid that you've. However, I am missing the so-what aspect?

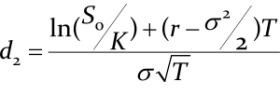

I know it is dancing in front of my eyes -- but how do I compute the PD using the results of computing the call price and the put price? In other words, how do I interpret the results in the context of computing the PD? To make things more concrete, I am referring to the results of the example on Slide 56.

In contrast, I think I do understand how you arrive at the PD (using the distance to default metric) using the KMV model.

--sridhar

I am watching your Credit A, Part 1 episode 7....I think I understand the Merton model for valuing the debt of a firm. I've also understood the mechanics of working the associated EditGrid that you've. However, I am missing the so-what aspect?

I know it is dancing in front of my eyes -- but how do I compute the PD using the results of computing the call price and the put price? In other words, how do I interpret the results in the context of computing the PD? To make things more concrete, I am referring to the results of the example on Slide 56.

In contrast, I think I do understand how you arrive at the PD (using the distance to default metric) using the KMV model.

--sridhar

{kind=link}