Hi,

I tried to search Model 3 but the search didn't come up with anything meaningful.

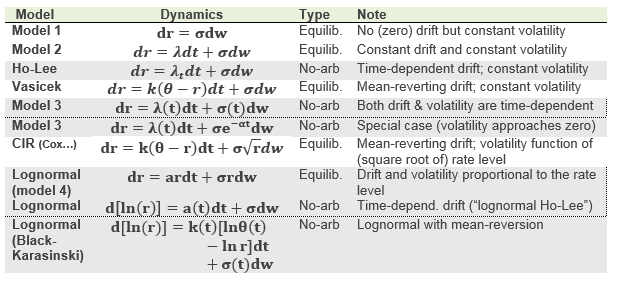

Models 3 and 4 both have an alpha factor in them, yet the text doesn't define what alpha is. So what does this alpha factor represent and are we expected to derive it on the exam or will it be provided? Thanks

I tried to search Model 3 but the search didn't come up with anything meaningful.

Models 3 and 4 both have an alpha factor in them, yet the text doesn't define what alpha is. So what does this alpha factor represent and are we expected to derive it on the exam or will it be provided? Thanks