sudeepdoon

New Member

Hi David,

I had a question and then a conern; first for the question:

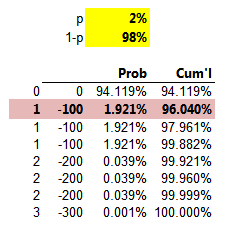

In the sheet we have got the VAR for a portfolio of 3 bonds as 100. I seem to have a different value..

When trying to see all possible outcome of the portfolio which would be 0,-100,-100,-100,-200,-200,-200 and -300 . The number of outcomes are 2^3 = 8...

On using the PERCENTILE function in Excel and trying to get a 95% VAR for the portfolio I get a value of 265..

Where am I wrong?

And for the concern:

Frankly, I dont seem to get a good hang of the ES and EVT. I have gone through the video and the AIMS are all clear but when it comes to understand the Excels things get hazzy... I guess you have it clear that this has a low probabilty to be questioned by still I dont feel satified (with what I have able to understand..)

For sure it would be a wrong expectation to ask you to give special attention to the topics. I request would be to please provide a link to any of for tutorials that may be taking a deeper dive into the topic or even a link to some article would also do.

Thanks,

Sudeep Manchanda

I had a question and then a conern; first for the question:

In the sheet we have got the VAR for a portfolio of 3 bonds as 100. I seem to have a different value..

When trying to see all possible outcome of the portfolio which would be 0,-100,-100,-100,-200,-200,-200 and -300 . The number of outcomes are 2^3 = 8...

On using the PERCENTILE function in Excel and trying to get a 95% VAR for the portfolio I get a value of 265..

Where am I wrong?

And for the concern:

Frankly, I dont seem to get a good hang of the ES and EVT. I have gone through the video and the AIMS are all clear but when it comes to understand the Excels things get hazzy... I guess you have it clear that this has a low probabilty to be questioned by still I dont feel satified (with what I have able to understand..)

For sure it would be a wrong expectation to ask you to give special attention to the topics. I request would be to please provide a link to any of for tutorials that may be taking a deeper dive into the topic or even a link to some article would also do.

Thanks,

Sudeep Manchanda

")

{kind=link}