David Harper CFA FRM

David Harper CFA FRM

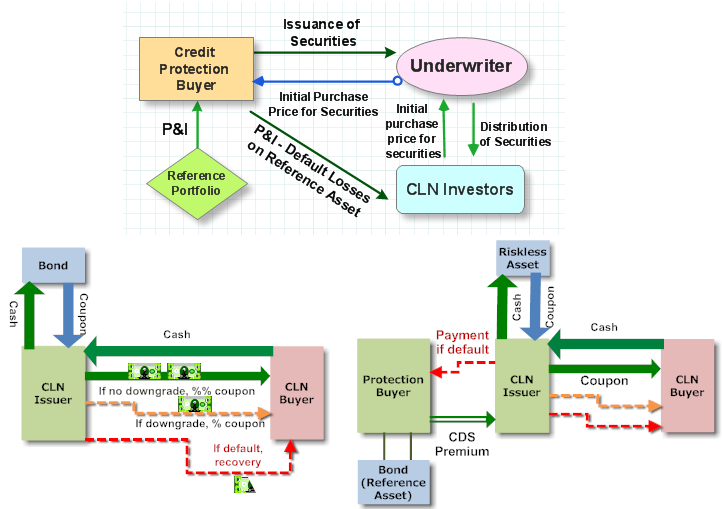

Hi @bpdulog Yes, the CLN buyer (aka, CLN investor, protection seller) is analogous to the CDS seller: without a default, this investor/buyer receives agreed-upon coupons and return of the principal at maturity. (this is the key difference between CDS protection seller, who has not funded the CDS and therefore only collects "coupon" premiums versus the CLN buyer who has funded the securities and so receives coupons but also expects to get their principal/par back at maturity). But, as you say, they have sold credit protection, so if there is a default, they have their coupons (interest) and principal at risk. However, just like the CDS protection seller, if a credit event happnes, pays only (if cash settlement) notional minus recovery, the CLN buyer is entitled to the recovered principal (or, analogously, if the CDS is physically settled, the protection seller pays the entire notional but they receive any recovered bond). In both cases, the actual loss is net of recovery and the protection seller is not protecting the entire principal (in the case of the CLN) or the entire notional (in the case of the CDS) but rather the actually lost portion (i.e., net of recovery). I hope that clarifies!

")