David,

Could you elaborate how it works?

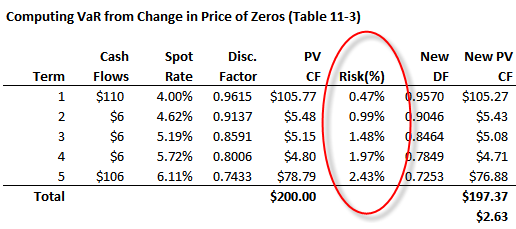

"The stress test consists of decreasing all bonds by their VaR"

Does it mean the portfolio's value is decreased by the total VAR? Any special point/concept this AIM trying to deliever other than aggregating each zero's VAR to get a total VAR?

Thanks.

Could you elaborate how it works?

"The stress test consists of decreasing all bonds by their VaR"

Does it mean the portfolio's value is decreased by the total VAR? Any special point/concept this AIM trying to deliever other than aggregating each zero's VAR to get a total VAR?

Thanks.

{kind=link}